Views: 0 Author: Site Editor Publish Time: 2026-02-28 Origin: Site

Advanced ceramics are an important branch of the new materials industry. The fields of high-strength structural ceramics and multi-property functional ceramics are expanding rapidly. Among them, functional ceramics account for approximately 75% of advanced ceramics, and high-precision electronic ceramics make up 80% of functional ceramics. Benefiting from the growth in high-end manufacturing market demand and new material industry policy incentives, the market size of electronic ceramics has steadily increased.

Electronic ceramics and miniaturized components are an important part of supporting the development of high-tech strategic industries. For instance, in fields such as 5G communication, artificial intelligence, new energy vehicles, industrial automation, and smart consumer electronics, the demand for high-performance and highly reliable electronic components is continuously increasing, and the market size has reached trillions of dollars. Several major production and manufacturing centers for electronic ceramics and components have emerged internationally, and competition is becoming increasingly fierce. As one of the global electronic manufacturing centers, China is facing challenges from international competitors. Therefore, it is necessary to continuously increase investment and research and development efforts in the field of electronic ceramics and components to enhance its competitiveness in the global market.

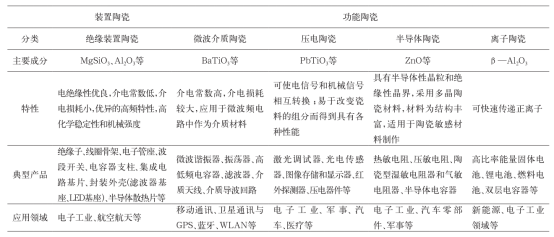

The definition and classification of electronic ceramics

Broadly speaking, electronic ceramics refer to "inorganic non-metallic materials that are processed through artificial refinement of inorganic powders, with specific structural design, precise chemical composition, appropriate molding-sintering integrated processes and firing procedures to achieve specific properties. After processing, they reach the dimensional accuracy required for use." These materials possess unique dielectric properties, electrical, optical, magnetic and other properties, as well as high hardness, wear resistance, and high fracture toughness, thus playing a crucial role in the fields of electronics, communications, automation, energy conversion and storage.

In terms of application, electronic ceramics can be classified into five categories: insulating device ceramics, fast ion conductor ceramics (ionic ceramics), semiconductor ceramics, piezoelectric functional ceramics, and high-dielectric constant capacitor ceramics. The main components, temperature stability characteristics, characteristics and main application fields of each type of ceramic are shown in the table below.

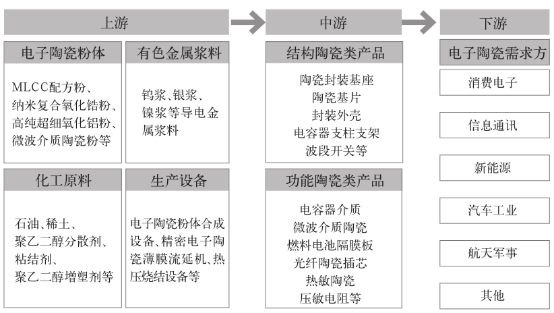

The upstream part consists of raw material and equipment suppliers. The raw materials involved mainly fall into three categories:

① Electronic ceramic powders such as high purity alumina and yttria-stabilized zirconia have been partially replaced by domestic products. However, there are still many types of electronic ceramic powders that cannot match the high performance foreign benchmarks (foreign counterparts) and are mainly imported.

② The pastes such as low-resistivity silver pastes and precious metal pastes are mostly imported.

③ Chemical products are mainly imported from American enterprises. The equipment used for manufacturing electronic ceramics mainly includes equipment for synthesizing nanoscale electronic ceramic powders, precision electronic ceramic film extruders, atmospheric-controlled hot-pressing and sintering equipment, laser cutting machines, etc. Some of these devices have already been domestically produced, reducing the dependence on imports.

The main participants of the midstream electronic ceramics manufacturing enterprises include foreign-funded enterprises, large state-owned enterprises, and small and medium-sized private enterprises. They mainly engage in the research and development, processing, and sales of electronic ceramic components and products. The enterprises involved in the midstream industrial chain are all capital-intensive and technology-intensive enterprises. During the research and production process, due to the relatively complex preparation process of electronic ceramics, achieving technological innovation breakthroughs requires the support of R&D technicians and high-precision automated equipment. During the preparation process, each link will affect the performance of electronic ceramic materials, and the industry barriers are relatively high. Therefore, scale-integrated management is needed to reduce costs.

The downstream mainly applies to terminal consumer electronics, information communication, automotive industry, new energy, aerospace and military sectors, etc. As one of the key strategic materials required for the development of China's new generation information technology industry, its application fields will continue to expand and the demand will keep increasing. The rapid growth of the downstream industry will drive the rapid growth of the demand for electronic ceramics-related components.

Compared with traditional materials, electronic ceramics materials possess advantages that traditional materials cannot match. Their application fields are constantly expanding and the market demand is continuously increasing. For instance, in the fields of computers, laptops, and tablet computers, to enhance the performance of products, electronic ceramics will inevitably replace some metal and plastic components, such as in MLCCs, thermistors, and piezoelectric ceramic speakers; in the communication field, with the widespread application of 5G technology, the trend of "Internet of Everything" will emerge, which will inevitably increase the demand for electronic ceramic components such as optical sensors, 5G communication parts, and crystal oscillators, along with ceramic antennas, RF filters, and microwave dielectric ceramics; with the arrival of intelligentization in the automotive industry chain, the automotive electronics industry is rapidly rising, and the demand for electronic ceramic components, including oxygen sensors, ceramic igniters, and piezoelectric ceramics for ultrasonic radar, is increasing. The rapid development of these related industries will directly drive the rapid growth of the market demand for electronic ceramics, spanning the entire industry chain from base materials to precision components.

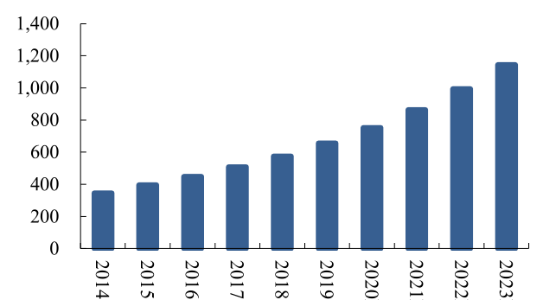

The market size of electronic ceramics in China has increased from 34.66 billion yuan in 2014 to 75.64 billion yuan in 2020, with a compound annual growth rate of 13.7%. The overall demand for electronic ceramic components is in an upward development phase. In the next five years, as the domestic substitution of imported products accelerates, the market size of electronic ceramics in China will continue to maintain a high growth trend. According to the budget of the institution, the market size of electronic ceramics in China is expected to reach 114.5 billion yuan in 2023.

l Miniaturization & Micro-miniaturization

To meet the demands of electronic information technology, the miniaturization and micro-miniaturization of devices have become a development trend. Various passive components based on electronic ceramic materials have put forward higher performance requirements, which is also the bottleneck restricting the realization of the miniaturization and micro-miniaturization of the entire machine. Currently, the market demand for miniaturized and micro-miniaturized electronic ceramic components is very large, such as chip-type multilayer thermistors, chip-type voltage-sensitive resistors, multilayer piezoelectric ceramic transformers, chip-type inductor-type components, and other examples like chip-type ceramic capacitors, chip-type EMI filters, and micro varistors. At present, chip-type functional ceramic components are the main part of electronic ceramic passive devices and a key segment within the broader electronic ceramics market, including advanced substrates and hermetic packaging ceramics. Therefore, strengthening the research on the miniaturization and micro-miniaturization of ceramic components is one of the key directions for the development of electronic ceramics.

l High-frequencyization & Frequency Seriesization

With the miniaturization and portability of communication terminal devices, the significance of high-performance microwave dielectric ceramics has become increasingly important. At the same time, there are higher performance requirements for microwave ceramic dielectric materials, as well as microwave resonators, microwave capacitors, and microwave filters, including key products like antenna duplexers, circulators, isolators, and high-frequency substrates. Therefore, the research focus in the field of new electronic components is to develop electronic ceramic materials with working frequencies ranging from high, medium, to low series.

l Integration & Modularization

With the development requirements of diversified functions, high integration, digitalization and low cost of electronic products, electronic ceramic components are bound to develop in the directions of miniaturization, functional integration, device combination and low cost, driving innovations in products like integrated passive devices (IPDs), RF modules, sensor arrays, and multi-layer ceramic packages. To achieve miniaturization and functional integration of electronic ceramics, the key lies in advanced heterogeneous material co-firing technology and low-temperature co-fired ceramic technology, which are fundamental to producing advanced LTCC (Low Temperature Co-fired Ceramic) substrates and multi-functional modules. This is currently an important research direction in the field of electronic ceramics.

l Functional Combinatorial & Diversification

With the intensification of competition in the information technology market, single-function electronic ceramic components have been unable to meet the performance requirements. Combining electronic ceramics with other materials (semiconductors, metals, etc.) to form composite electronic ceramics to meet the application needs of electronic components in different fields such as MEMS devices, flexible electronics, structural electronics, and bio-medical sensors has become an inevitable trend in the development of electronic ceramics. Therefore, strengthening the development of composite electronic ceramics is one of the current research focuses, which provides important technical support for the deviceization of electronic ceramics and enables advanced hybrid systems like piezoelectric-semiconductor composites and ceramic-metal integrated components.

l Lead-free & Environmentally Friendly

To meet the requirements of sustainable development and environmental protection of human society, the development of environmentally friendly electronic ceramics has become one of the key focuses in the research of electronic ceramic materials. For instance, developing non-lead piezoelectric ceramics such as those based on potassium sodium niobate (KNN), bismuth sodium titanate (BNT), or barium titanate systems to replace the current zirconate titanate lead-based system holds great significance for applications in eco-friendly actuators, energy harvesters, and green sensors.

Due to the high technical barriers in the production of electronic ceramics including key materials like high-purity alumina powder, specialized ferrites, and dielectric formulations, this industry has long been monopolized by companies from the United States, Japan, and Europe. Although some of the electronic ceramics in China have reached the international advanced level in terms of theoretical research and experimental capabilities, compared with economic developed countries such as those in Europe and Japan, they are still at the initial stage and have broad development potential. Currently, compared with foreign countries, the problems and gaps existing in China's electronic ceramics industry mainly include the following four aspects relating to advanced manufacturing of components such as high-frequency filter chips, precision piezoelectric transducers, and multi-layer varistors.

l Shortcomings in the technology for preparing high-end powders

In the process of preparing electronic ceramics, the quality of the powder is crucial. The main bottleneck restricting the development of China's electronic ceramics industry is the technology for preparing high-purity, high-performance and ultra-fine ceramic powders suitable for applications in MLCC dielectrics, piezoelectric actuator materials, and advanced semiconductor packaging substrates.

Currently, Japan is the largest producer of electronic ceramic powders globally (with approximately 65% market share).

From the perspective of global market share, the technology for preparing high-end electronic ceramic powders in China has not yet been fully breakthroughed. It mainly relies on imports. For instance, for 99.99% high-purity alumina powder used in ceramic substrates, spark plug insulators, and wear-resistant coatings, the alumina powder produced by Japanese enterprises can be sintered at 1300℃, while the sintering temperature of domestic enterprises needs to be above 1600℃; for high-purity silicon nitride powder essential for high-temperature engine components, bearing balls, and cutting tools, it is still restricted by some companies, and efforts are urgently needed to improve the consistency of powder quality in research and development.

l The manufacturing equipment for electronic ceramics needs to be improved.

Although our country can introduce advanced foreign electronic ceramic manufacturing equipment to enhance the production technology level, the investment amount is huge, which to some extent restricts the development of the domestic electronic ceramic industry. Additionally, the domestically produced manufacturing equipment for electronic ceramics in our country is mostly of the imitation type, and the key production technologies have not yet been fully mastered, resulting in a decline in the reliability and consistency of some electronic ceramic products such as multilayer varistors, high-frequency filters, and piezoelectric actuators, making it difficult to compete with similar foreign products. Therefore, the manufacturing level of electronic ceramic equipment in our country is one of the key factors restricting the development of the domestic electronic ceramic industry.

l The efficiency of the new product industry's transformation is low.

There are over 200 types of ceramic materials and 2,000 types of application products worldwide. For the domestic electronic ceramics industry, the vast majority are still at the laboratory stage, and there is a considerable gap from the industrialization goal. The organic combination of industry, academia and research has not yet been achieved. Additionally, some products are difficult to popularize due to issues such as production costs and reliability. Therefore, China needs to accelerate its pace of catching up in the research and application of new products.

l The industry lacks large-scale leading enterprises.

There are over 300 electronic ceramic-related enterprises in our country, but the majority are small and medium-sized micro-enterprises (accounting for approximately 70%), with products being relatively monotonous, high production costs, and lacking market competitiveness. Additionally, during the research and development process, there is a lack of independent innovation; the adoption of a laissez-faire development approach has led to overcapacity in product production. For instance, in recent years, there has been an oversupply of foam ceramics and ceramic cutting tools, causing some small and medium-sized enterprises to struggle to survive and even go bankrupt.

At present, the global electronic ceramics market is mainly dominated by foreign electronic ceramics manufacturers.

From the perspective of technological innovation, the key core preparation technologies for electronic ceramic materials such as advanced tape casting, multilayer co-firing, and precision micromachining for components like SAW filters, LTCC modules, and piezoelectric transducers are still controlled by manufacturers from Europe, the United States, Japan and South Korea. In terms of market share, Japanese enterprises produce the most types of electronic ceramics, have the best overall performance, the widest application fields and the largest output. They hold a significant lead in the global electronic ceramic market (accounting for approximately 50% of the share); the United States has a slightly slower development process for electronic ceramic industries and accounts for about 30% of the global electronic ceramic market share, ranking second; the European Union places greater emphasis on the development of energy-saving and environmentally friendly electronic ceramic materials for applications in solid oxide fuel cells, thermal barrier coatings, and bio-ceramic sensors, and its share of electronic ceramics is approximately 10% of the global market share.

The electronic ceramics industry in our country started relatively late and still has a considerable gap compared to economic developed countries such as the United States and Japan. There is still a long way to go in terms of the research and development of electronic ceramics.

(1) Strengthen national policy support. The core technologies of enterprises in China's electronic ceramics industry are mainly dependent on imports, lacking certain independent innovation capabilities. This will inevitably restrict the development of enterprises and make it difficult to enhance their product market competitiveness. Therefore, China should further strengthen policy support for the development of electronic ceramics, enhance the attractiveness of domestic capital, increase support for research and development funds, cultivate Chinese brands, implement the strategy of large companies, and promote the growth and expansion of domestic related enterprises.

(2) Strengthen basic research and innovation, enhance international competitiveness, increase investment in researchers and funds, overall strengthen research and development capabilities, strengthen direct contact and collaboration among various research units, create a comprehensive research and development body based on new material research and with a strong background and research ability in device application research focused on areas such as thin-film ferroelectrics, high-Q microwave ceramics, and flexible piezoelectric composites; establish an effective mechanism that can promptly and effectively transform achievements and specifically realize the combination of "industry-university-research" cooperation.

(3) Coordinate the planning of upstream and downstream enterprises in the electronic ceramics material and component industry chain spanning from dielectric powders and ferrite cores to advanced substrates and integrated functional modules, strengthen the raw material supply chain to ensure the supply of high-purity and high-stability electronic ceramic precursors like barium titanate, zinc oxide, and lead zirconate titanate alternatives, vigorously carry out the research and development of high-end process equipment for fine-patterning, precision sintering, and automated assembly, strengthen independent innovation in passive components such as chip inductors, EMI suppression filters, and temperature-compensated crystal oscillators and overall equipment design, and strengthen the construction of relevant standards.

Q1: What are the main "critical bottlenecks" currently faced by the Chinese electronic ceramics industry?

A1: The main bottlenecks lie in the high-end powder preparation technology and core manufacturing equipment. High-purity and ultra-fine high-end ceramic powders (such as 99.99% high-purity aluminum oxide) are mainly imported from Japan; meanwhile, although some high-end manufacturing equipment (such as precision extrusion machines and laser cutting machines) has been partially domesticated, the key technologies and reliability still fall short of those in foreign countries, resulting in insufficient performance of high-end products.

Q2: What are the key future trends in electronic ceramics?

A2: The article points out five main directions:

Miniaturization: 1.Meeting the demand for miniaturization of electronic devices (such as miniaturized MLCC).

2. High Frequency: Meeting the high-frequency requirements of 5G/6G communication.

3. Integration: Implement passive integrated modules through technologies such as LTCC.

4. Combinatorial Approach: Integrating semiconductor, metal and other materials to meet multi-functional requirements.

5. Environmental friendliness: Develop new types of ceramic materials that are lead-free and environmentally friendly.

Q3: What are the main downstream application fields of electronic ceramics?

A3: It mainly covers communication (5G base stations, filters), consumer electronics (MLCC in mobile phones and computers), automotive industry (sensors and radars for new energy vehicles), and high-end manufacturing fields such as aerospace. Among them, 5G and new energy vehicles have been the main growth drivers in recent years.

Q4: What are the problems existing in the enterprise structure of China's electronic ceramics industry?

A4: The industry lacks leading enterprises with international competitiveness. Currently, there are many related enterprises in the country (over 300), but approximately 70% of them are small and medium-sized enterprises. Their products are monotonous, costs are high, and they mostly concentrate in the mid-to-low end market. They are facing overcapacity issues, while the high-end market is still dominated by foreign enterprises.

Please contact us anytime should you require more information.